Brent Cassity book Nightmare Success fact-check

Brent Cassity book Nightmare Success fact-check

Recently, Brent Cassity, who has finished his prison sentence at the U.S. Penitentiary in Leavenworth, published a book of his memiors. The book, Nightmare Success, contains numerous statements and accusations that we think deserve closer examination.

Is his book, Nightmare Success, an accurate depiction of his role in the fraud?

Read on and decide for yourself.

Brent has written his book with a narrative that he was an innocent man caught up in a major fraud. Is the book at all accurate? We will show excerpts from the book and present some statements with evidence to back them up. And, we have a lot of evidence. From there, you can form your own opinion of what the true story is. This is a matter of public interest and we have no motivation other than to publish the facts behind the story of a key player in one of the largest and complicated frauds in our country’s history. For more about us and the motivation behind this site, please see the About page.

Above: Brent Cassity, his wife, and two of his daughters leave the Federal Courthouse in St. Louis, Missouri after Brent was sentenced to a 5-year prison term in Leavenworth. Photo Credit: Robert Cohen / St. Louis Post-Dispatch / Polaris © 2013 St. Louis Post Dispatch. Reused with permission.

In the book, Nightmare Success, Brent Cassity lays blame on almost everyone but himself and attempts to tell a story that would leave one to feel sorry for the man. However, many of his assertions deserve to be challenged.

For those of you who haven’t read it, here’s a recap of the book that we borrowed with permission:

I’m innocent!

It was our corporate attorney’s fault, my criminal attorney’s fault, our competitors’ fault, my friend’s fault, our actuary’s fault, the whistleblower’s fault, our employees’ fault, our ex-employees’ fault, the state regulators’ fault, the prosecutor’s fault, our executives’ fault, the reinsurer’s fault, and my dad’s fault. Oh, did I mention I was innocent?

The End.

Below we will display excerpts from Brent’s book and then provide some commentary and supporting documentation.

Brent has a common theme throughout the chapters discussing National Prearranged Services (NPS) that he was not active in the insurance part of the operation until 2007 and that it was “his dad’s area.” From the book:

From Chapter 30: 2007 – The Beginning of a Nighmare

Page 113: “We owned an insurance company. I always hated math in school and my college major, political science, magically did not require math courses. I stubbornly looked at the insurance operation as a necessary safeguard to fund our preneed sales contracts. That was dad’s side of the company.”

And From Chapter 31 – The Thunder of the Crisis

Page 116: “I didn’t carry an official title in either Lincoln Memorial Life or NPS…”

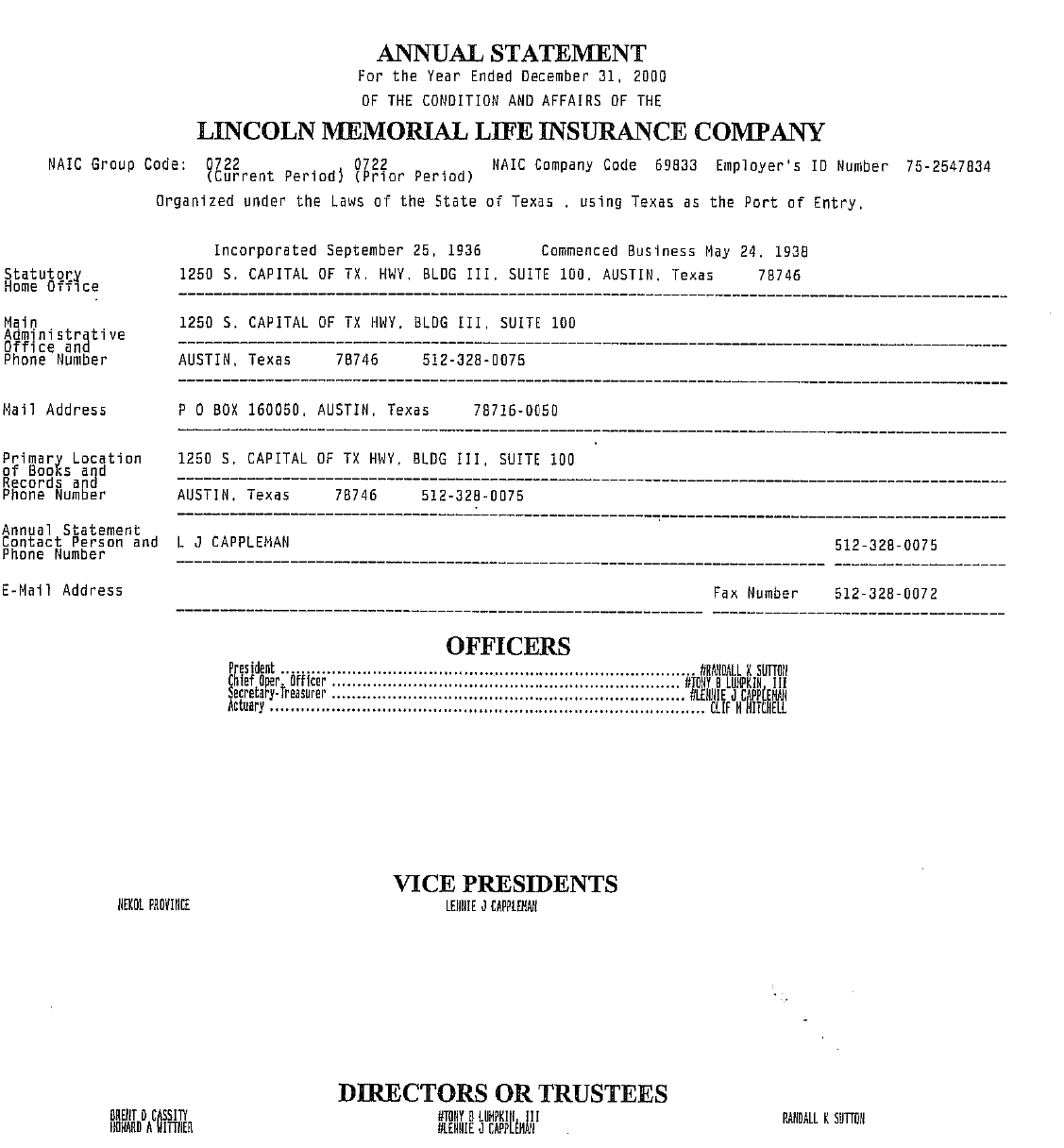

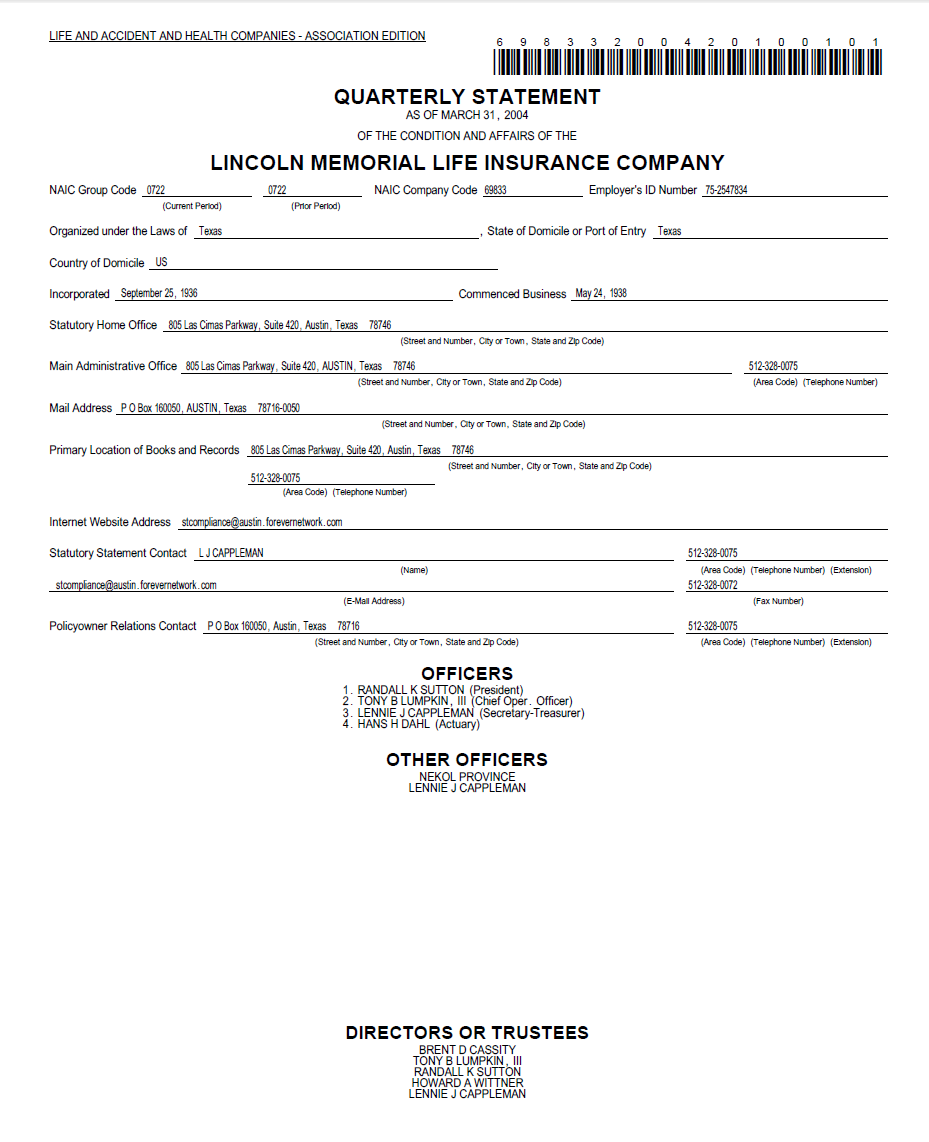

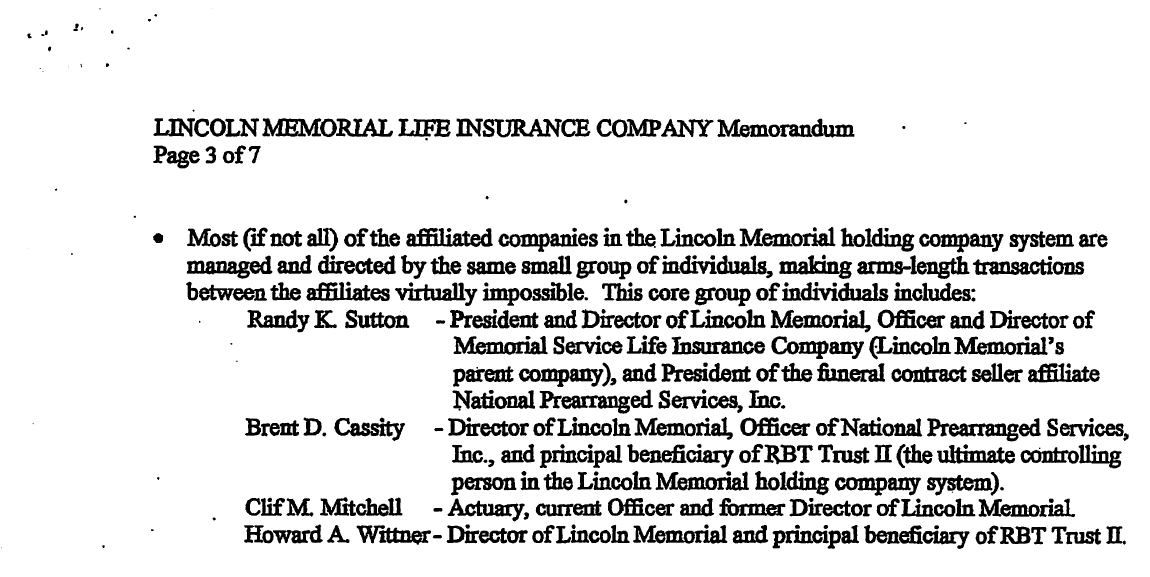

Didn’t carry a title with Lincoln Memorial Life? Interesting, because he was Chairman of the Board of Directors for Lincoln Memorial Life and had been for at least 7 or 8 years.

So, let’s see:

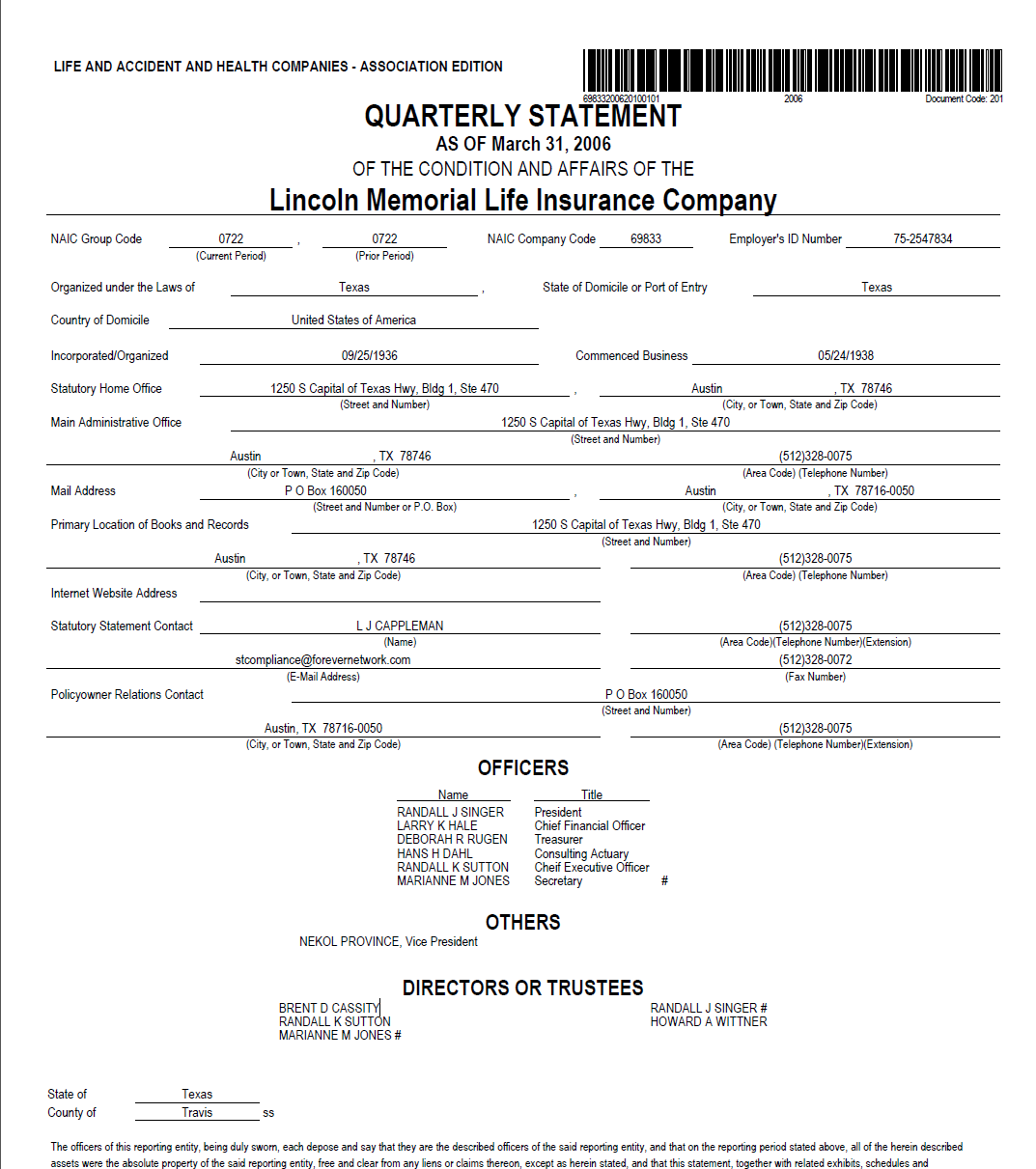

Oh, here’s that documentation we promised: Here are links to copies of the Annual Statements for Lincoln Memorial Life that shows Brent on the Board of Directors in 2000, 2004, and 2006. (The statement for the year 2000 reflects that he was appointed sometime before January 1, 2000.)

Brent claims throughout the book that he didn’t know about the insurance side of the business and wasn’t involved until the very end when his dad put him in the line of fire to defend the Company to the regulators. As a board member, he signed board minutes, received financial statements, received and sent numerous emails about the insurance operations, and attended countless meetings. We have dozens of emails showing that Brent was involved in insurance matters dating back to 2002. (We don’t have access to any emails prior to that year.)

Don’t take our word for it. Here are just a few samples of the emails over the years showing his involvment in the insurance company:

2002 Brent scolding insurance employee over agent licensing issues

2004 Brent opining on the importance of a highly rated reinsurance company

2005 Brent making calls on who attends meeting with the Texas Dept. of Insurance

2005 Brent making the call on reinsurance deal as a result of a consumer complaint

2006 Brent involved in Hannover Reinsurance dispute early on in the discovery process

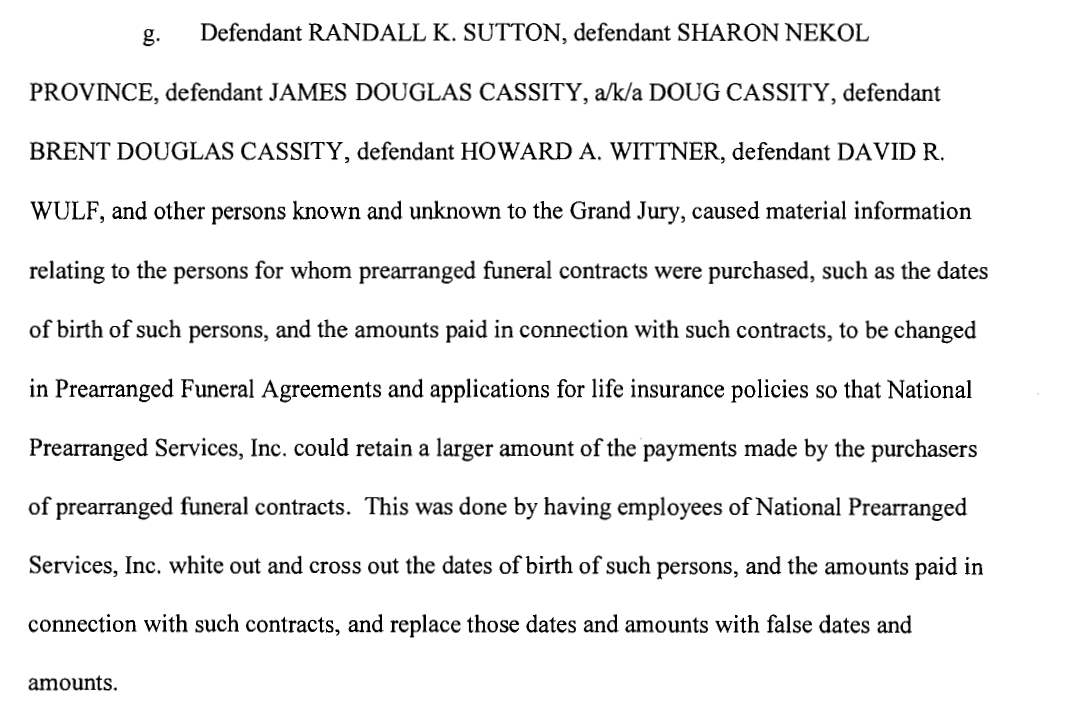

A key part of the Ponzi scheme involved the changing of payment terms and dates of birth on insurance applications. Thousands and thousands of applications were illegally altered using white-out. One office supply company made a comment that NPS went through more white-out than all of their other St. Louis customers combined. By 2007, the practice was rampant.

From the book, Nightmare Success:

From Chapter 31 – The Thunder of the Crisis

Pages 118-119: “I was having a meeting with Dad in his office, when Kati knocked on the door and came in. When Katie [sic] was nervous or stressed, hives would break out on her neck. She had hives.

“We have a problem with our Ohio paperwork,” she said.

I knew that all of our contracts and forms were approved by each state we operate. How could we have a paperwork problem?

She explained that where had been a white out problem on our policies.

“What?” I said.

It appeared to be laziness in the department that was managed by Tony Lumpkin.

Kati explained that in the state of Ohio all the rights and benefits were assigned to NPS because NPS was the responsible party to pay for the funeral at the time of need. There was a line on the contract for the beneficiary of the policy. That line was supposed be filled out by the funeral director to be NPS, and sometimes they put the funeral home name by mistake. Our staff’s job was to correct the mistake by adding an addendum sheet attached to the policy. Instead, the staff had used white out to make the correction.

I was furious. It was a self-inflicted wound at the exact moment we needed the trust of our Ohio Funeral Directors. Dad told Kati we were going to send a letter to the funeral directors explaining exactly what happened. Now matter what, using white out on policies sounded horrible.

The U.S. Attorney’s office did not file criminal charges because of clerical errors. Policy applications (not policies as Brent states) were whited-out by the tens of thousands. It was a deliberate and systematic FRAUD.

We can’t say that the error Brent mentioned didn’t happen, but clerical errors weren’t the problem as far as Ohio – or the U.S. Attorney’s Office – was concerned. They changed dates of birth in order to defraud their own insurance company and the reinsurers by paying lower premiums and receiving higher commissions. They changed payment information so they could hold on to the funds and not pass them to the insurance company. It was systematic and, by this time period, was done to thousands of policy applications as a desperate move to keep the Ponzi alive. Oh, by the way, much of this went on for years in an office just a few steps away from Brent’s office on the exclusive 5th floor of their corporate offices in St. Louis.

Here’s an excerpt from the federal indicment discussing whiting out and changing birth dates and amounts on policy applications.

But Wait, There’s More…

As spelled out in great detail beginning on paragraph 100 in pages 32-37 of the civil complaint, NPS went through great troubles to hide the white-out fraud from their own sales force and funeral homes. On February 11, 2008, in response to an e-mail from an NPS sales agent asking whether NPS engaged in policy mismatching, Brent Cassity wrote to the head of his NPS Advantage sales team, Roxanne:

“Just tell her that is not being done..”

Again, we promised we’d let you draw your own conclusions regarding Brent’s involvment in the fraud so we’ll refrain from commentary and let you decide.

Brent references the Hannover arbtration case multiple times in his book. Hannover, a large reinsurance company, had filed an arbitration case against the Cassity companies alleging fraud. Brent makes claims that his dad and the corporate attorney kept the facts hidden from him.

From the book:

From Chapter 31 – The Thunder of the Crisis

Page 116:

“I received another ominous phone call from Singer. Someone was leaking documents from our office and Singer suspected who it was. He feared the sealed document of our arbitration with Hanover [sic] was among them.”

Page 117: [from a meeting with Mr. Larson from the Ohio Dept. of Insurance]

“Mr. Larson didn’t waste any time. Their department had received a copy of the sealed arbitration from Hannover that alleged fraud and breach of contact. Singer had been right about the office leaker. This immediately put us on defense with something that we had not planned on discussing. Frank Larson told us that if we lost this arbitration our insurance company could potentially become insolvent.”

“When we took a break, I called Dad who had returned from Africa.”

“‘This is some serious shit going down in Ohio,’ I said. ‘I have a room full of regulators sitting on this meeting wanting to eat our company alive. And, on top of that, we have a mole in our Austin office. They have the Hannover documents from the sealed arbitration.'”

Brent uses the word “sealed” multiple times when referring to the Hannover arbitration. The documents were not “sealed” or secret in any way. In fact, Lincoln would have been required to give the arbitration documents to regulators themselves as a part of any examination. It is a crime to mislead regulators or withhold documents, especially of that of that magnitude. Of course, Brent would find this out the hard way down the road….

If your business’ survival relies on withholding documents from regulators, maybe it’s a good time to ask yourself a couple of questions.

Later in the book, Brent blames his dad and the corporate attorney, Howard Wittner for not settling on the Hannover arbitration. Here’s an email from Brent showing his desire to get more agressive with the Hannover arbitration early on in the discovery process. Then, a few chapters later, Brent blames regulators for taking down the Company before the arbitration panel announced its decision.

Another key part of the scheme was policy loans. Again, Brent claims to “not fully understand” them and that was all a part of “dad’s part of the business.” Here is an excerpt from the book and then we’ll take a look at some facts. This would have been around 1999 or 2000. Brent had just been turned down for a deal to sell the insurance company and the reason given by the potential buyer was policy loans.

From Chapter 24 – Acquisition Idea

Page 99:

“Mitch said, ‘The reason we didn’t do a deal with your insurance company was because Larry said your policy loans of $13.5 million are too high.'”

“I didn’t fully understand how policy loans worked, but when I got back in town I asked Randy Sutton what would be the easiest way to wipe them out. He told me that about $80 million in preneed annual volume would do it. Since, I knew that we would probably grow through that number by the following year I never revisited that issue with Sutton, again. That oversight would change my life beyond anything I could have imagined.”

Oversight? It’s hard to know where to begin on this one. The Cassity companies started taking policy loans in 1995. The book excerpt above was in 1999 or 2000 based on the timeline in Brent’s book. Let’s start by jumping forward and taking a look at policy loan balances as of August, 2006. To the right is a chart of loan balances grouped by state or trust. Take note of the line for loans taken out by the Mt. Washington Cemetery, which, even by Brent’s own words, he managed directly and exclusively. By the end of this fraud, over $116 million in policy loans will have been looted from the insurance company.

So, just so we’re clear, you are the C.E.O. of a company that has borrowed tens of millions of policy loans, and you claim you “didn’t fully understand” how they worked?

Policy loans are not a difficult concept to understand. Whole life policies have equity referred to as cash value. You can borrow against that cash value just like you can borrow against the equity in your home. Of course, when the policy is cancelled or there is a death claim against it, the insurance company reduces the refund or claim amount by the loan balance. It’s just like if you sold your house and the mortgage company gets paid before you do. So, in the above case, the insurance company would be holding back $62.5 million dollars against future claims (with interest accumulating at 8%.) This means that when NPS or the cemetery had a client holder file a death claim, they would have to pay the full amount while only receiving the claim amount minus the policy loan from the insurance company. The policy loan repayment could often reduce the death claim by more than 50%. It doesn’t take a rocket scientist to see this just might be a problem….

This one piece of the fraud was enough to take down the entire Cassity conglomerate all by itself.

So, to recap:

We can’t upload all of the data required to calculate the above policy loan balance but have it available to anyone who requests it to verify our numbers. Here is a excerpt of an internal memo at the Missouri Department of Insurance dated August, 2001, reflecting that Brent was also an officer of NPS.

We are curious how Brent would explain his response to this email from Nicki Province, who ended up going to prison herself. Nicki wrote this email in 2007 to Brent following questions by NPS sales agents and funeral homes in Ohio regarding policy loans:

Nicki Province: “The answer should simply be, we do not do policy loans in any state… If the ae (account executive or sales agent) is asked if we ever have the answer should be “not that I am aware of.”

Brent Cassity’s reply the same day: “Agreed”

So, here we have Brent agreeing to tell the salesforce that the company does not do policy loans. It seems he’s more willing to lie than most politicians. It’s all spelled out in more detail starting at the top of page 43 of the civil compaint.

If you find that it’s necessary to tell your salesforce that you don’t do policy loans when you in fact have done thousands and thousands, maybe it’s another one of those times you should ask yourself a couple of questions…

Throughout the book, Brent talks of PLICA (a medical malpractice insurance company that he, his dad, the corporate attorney, and another partner had acquired) like it could have been the savior of the Cassity enterprise and that it could be sold for tens of millions. From the book below –

Chapter 31, The Thunder of the Crisis, page 119:

“I thought we should sell our medical malpractice insurance company PLICA, a thriving company that had over $18 million dollars in reserves and over $28 million in capital and surplus. It was licensed in thirty-five states and was writing over $40 million a year in premiums. Even in a fire sale, it could be sold for $75 million. This would shore up our capital and surplus in Lincoln, and give us needed operating capital to survive.”

In truth: When it came to PLICA, there was fraud under every stone.

PLICA was dead before they ever even wrote their first piece of business. The numbers Brent quotes above are true – as they were reported to the State of New York, where PLICA was domiciled. Those numbers would seem to indicate a healthy, thriving company as Brent descibes it. Trouble is, as revealed in the indictment and by interview notes, the Cassity’s application to buy PLICA and the PLICA financials themselves contained false and misleading statements. It was only a matter of time until the regulators figured it out. According to the federal indicment, they also broke the law by using $4,600,000 from one of the Missouri preneed trusts to purchase PLICA.

As described in one auditor’s interview with the FBI, Postal Inspector, and the IRS, New York had tipped Missouri off that something was wrong months before the regulators actually took it over. They had failed to disclose transactions that they were required to disclose, they had created a “special” financial statement just so the application to make the purchase would look more appealing. Also according to the auditor, they were also bleeding as much money as they could from the Company by paying high salaries and inflated administrative costs. It was their opinion, that had the financial statements been reported accurately, PLICA was insolvent. These are just some minor points that Brent left out of his book.

This is all spelled out starting on page 1 of the notes from the FBI interview with the examiner from Missouri and on numerous pages throughout the Federal indictment.

Here’s an article with more information on Brent’s involvment with PLICA: New York Demands $10 Million from Execs

Well, there’s more. A lot more. Unfortunately, we’ve run out of time to spend on this for now. We’re going to highlight more of the book in the coming weeks in the form of blog articles. Check out our Blog section for updates!

For more interesting reading, check out the responses to the book from two of the individuals named in Brent’s book who at times worked with him:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}